UTI AMC group

UTI AMC group

India After COVID-19

07 April, 2020

Despite the tremendous suffering and confusion that consumes the world at present, we all knowthat at some stage, humanity will convincingly prevail over the virus. Every country is formulating its own unique response to the situation, one that delivers an optimal trade-off, in the context of its Socio-Economic-Political pressures. Recognizing the severe economic consequence to this virulent pandemic, the IMF has declared that the world is now in recession. For investors, the key concern would be the characteristics of the economic landscape we inherit, once the dust settles. Prime Minister Modi has ordered a 21 day countrywide lockdown, until 14th April, to prevent the transmission of the infection. This lockdown, which may well be extended, is saving lives on one hand but on the other hand, is destroying jobs and incomes. It is impossible to estimate the scale and nature of economic destruction, given the multiplicity of variables, not the least of which is the fiscal and monetary stimulus. While some domestic consumption will be destroyed in the short term, most will simply get deferred by a few months. Services sectors (Transportation, Tourism, Entertainment, Hotels) will be particularly afflicted but the rest of the economy should gradually recover.

Why India ?

The investment case for India has only strengthened in the current circumstances:

1. Relative advantage

India’s primary attraction as an investment destination has been its growth advantage, relative to most Emerging Markets and indeed all developed markets. This edge comes from having an economy predicated on Domestic Consumption by a large and young middle class population. Despite the global slowdown, this relative advantage remains intact. Countries that largely depend upon exports will suffer in a slowing environment. When IMF forecast the world average growth to be around 3%, India was growing at 6%. With IMF now forecasting a global recession for 2020, India will slow down to around 3% to 3.5%. Thus India will continue to deliver a growth much higher than the global average, making it a compelling equity market in the post-Covid world.

2. Subdued Oil

Oil price has had its worst quarter ever with prices falling by 65% in the face of collapsing demand. As economic activity flounders, it is expected that by July’20, the world will run out of storage capacity for crude oil. Such low prices signal a momentous boost for India, the third largest oil importer in the world. We estimate that India’s current account deficit for this year would be near Zero, as crude prices continue to plummet. Consequently, the Indian government will have significantly greater latitude in designing a formidable stimulus package for the domestic economy

3. Plan B for global manufacturing

The disruption of global supply chains unleashed by the Trade Wars, has only been exacerbated by the pandemic. The factory shut-down in China has imperilled global manufacturing across a multitude of sectors. This has forced an increasing number of companies to diversify their global manufacturing bases. India, having improved considerably its Ease of Doing Business score in the past few years, has emerged as one of the main contenders in this search for Plan B.

Global Debt Bubble

A striking feature of Indian economy is the low level of Public Debt to GDP (69%), compared to the rest of the world. The global Debt to GDP reached an all-time high of 322% in Dec’19 making debt servicing a huge challenge. In March’20, the yield on the 10 year US Treasury bond, for the first time in history, declined below 1%. This will only get worse with increasing unemployment and escalating fiscal stimuli.

There will be second order consequences of rising corporate defaults, particularly in the High Yield segment. While governments can print more money, businesses and households do not have that option. Some businesses might get bailed-out at the taxpayer’s expense but the widespread job losses will damage consumptiont trends, particularly in the highly leveraged societies. Again, in sharp contrast to the rest of the world, India’s household debt is minimal and a probable catalyst for the ensuing economic recovery.

Indian Markets

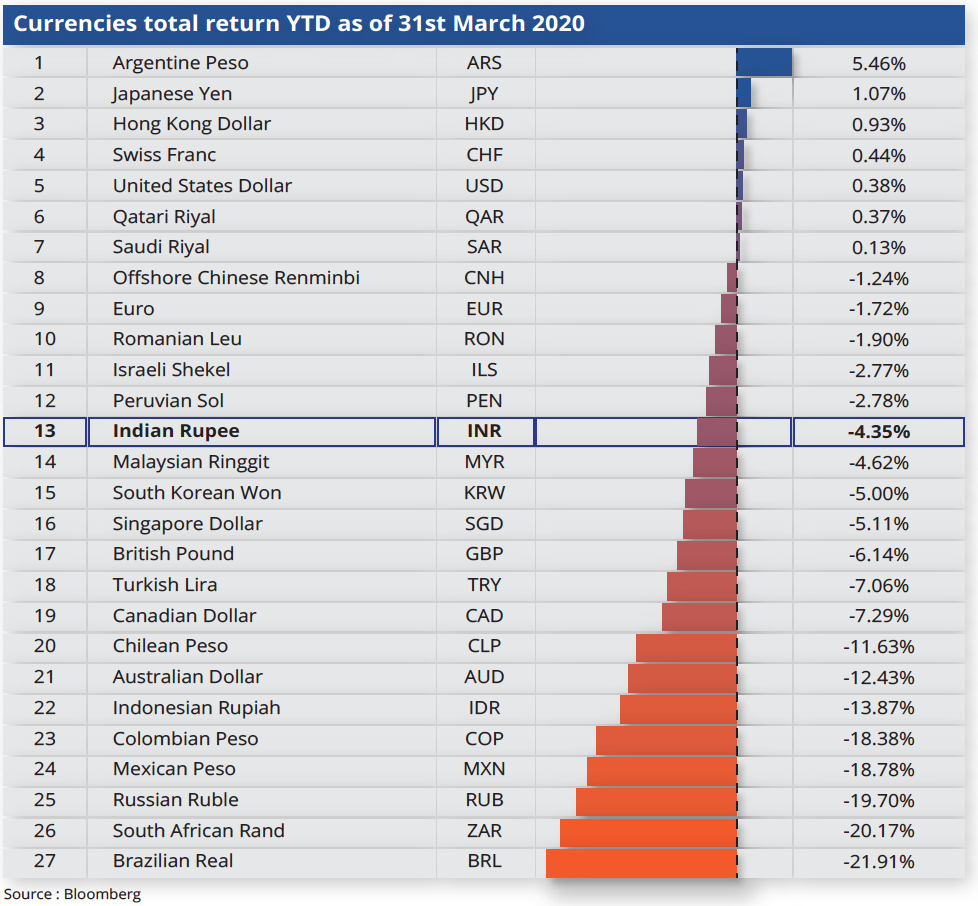

The S&P 500 has suffered its swiftest descent into a bear market on record, taking just 16 days to slump from all-time highs and end an 11-year bull market. The Indian market has been no different. This unprecedented erosion of global wealth has triggered a massive Risk-Off trade with investors abandoning Emerging Markets, in their quest for Liquidity and Safety. Global investors withdrew almost USD 16 billion from India (Debt & Equity combined) in March’20 alone, as against a total inflow of USD 12 billion in all of 2019. The PE ratio (Price to Earnings) of BSE 100, a prominent Indian index has crashed from nearly 26 to 15.5 in Q1 2020, bringing it almost to the levels last seen in 2008. A vast majority of the foreign investment in Indian equities happens through ETFs and these funds have witnessed the severest redemptions. Selling pressure globally has also originated from algorithmic traders where the programs have hit stop losses, activating margin calls and triggering a vicious cycle of further selling. Global risk appetite tends to swing erratically until a narrative of certainty takes shape. We know from earlier corrections that once a degree of normalcy returns, India’s appeal as a growth market brings investors flooding back. This coupled with the expectation that MSCI is considering to increase India’s weightage in the EM Index in its Aug’20 review, makes the coming weeks a buying opportunity. The turmoil in the global equity and bond markets has had its impact on the currency markets as well, asinvestors have scrambled to seek the safety of the US Dollar. Businesses and banks have bought USD in such quantities that the greenback has clocked its sharpest rise since

The document does not constitute an offer for share/units and is neither a recommendation nor statement of opinion or an advertisement. It does not constitute any prediction or any representation of likely future movements in rates or prices of any securities. The content of the statement above are for information purpose only without regard to the specific objectives, financial situation and particular needs of any specific person who may receive this statement. Users of this document should seek advice regarding the appropriateness of investing in any securities, financial instruments or investment strategies referred to on this document. This document has not been reviewed by the Monetary Authority of Singapore 2008. The Real Effective Exchange Rates (REER) index of EM currencies-ex China has already fallen below the 2008 levels. We are fast approaching values reminiscent of the Asian currency crisis of 1998. Even the GBP has witnessed a roller-coaster ride, falling by more than 6% this year. In contrast, the Indian Rupee has been reasonably stable, owing to its inherent structural strength.

Important Legal Information

The document does not constitute an offer for share/units and is neither a recommendation nor statement of opinion or an advertisement. It does not constitute any prediction or any representation of likely future movements in rates or prices of any securities. The content of the statement above are for information purpose only without regard to the specific objectives, financial situation and particular needs of any specific person who may receive this statement. Users of this document should seek advice regarding the appropriateness of investing in any securities, financial instruments or investment strategies referred to on this document. This document has not been reviewed by the Monetary Authority of Singapore